Asymptotic distributions

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

import seaborn as sns

import scikits.bootstrap as boot

The canonical case

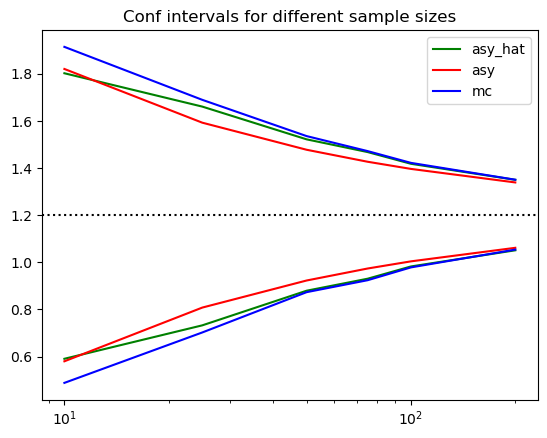

We simulate a linear model with normal errors, we compare the finite sample distribution to the asymptotic distribution.

def ols_normal(beta,X,N,e_sd):

""" Simulates the errors, estimates OLS coefficient, se, tstat and CI"""

E = e_sd*np.random.normal(size=N)

Y = beta*X[0:N] + E

cov = np.cov(Y,X[0:N])

beta_hat = cov[0,1]/cov[1,1]

beta_se = (Y-beta_hat*X[0:N]).std()/(np.sqrt(N)*X[0:N].std())

tstats_asy = (beta_hat-beta)/beta_se

ci_asy = beta_hat + beta_se * np.array([-1.96,1.96])

return({

'beta':beta_hat,

'se':beta_se,

'tstats_asy':tstats_asy,

'ci_lb':ci_asy[0],

'ci_ub':ci_asy[1],

'N':N})

beta = 1.2

R = 10000

e_sd = 1.0

X = np.random.normal(size=200)

res = [ols_normal(beta,X,N,e_sd) for _ in range(R) for N in [10,25,50,75,100,200]]

sim = pd.DataFrame(res)

# append theoretical asymptotic CI

sim['ci_lb_asy'] = beta - e_sd*1.96/np.sqrt(sim['N'])

sim['ci_ub_asy'] = beta + e_sd*1.96/np.sqrt(sim['N'])

sim_tmp = sim.groupby('N').mean()

sim_tmp['ub'] = sim.groupby('N')['beta'].quantile(0.975)

sim_tmp['lb'] = sim.groupby('N')['beta'].quantile(0.025)

sim_tmp = sim_tmp.reset_index()

plt.plot(sim_tmp['N'],sim_tmp['ci_lb'], color="green", label="asy_hat")

plt.plot(sim_tmp['N'],sim_tmp['ci_lb_asy'], color="red", label="asy")

plt.plot(sim_tmp['N'],sim_tmp['lb'], color="blue", label="mc")

plt.plot(sim_tmp['N'],sim_tmp['ci_ub'], color="green")

plt.plot(sim_tmp['N'],sim_tmp['ci_ub_asy'], color="red")

plt.plot(sim_tmp['N'],sim_tmp['ub'], color="blue")

plt.axhline(beta,linestyle=":",color="black")

plt.legend()

plt.title("Conf intervals for different sample sizes")

plt.xscale('log')

plt.show()

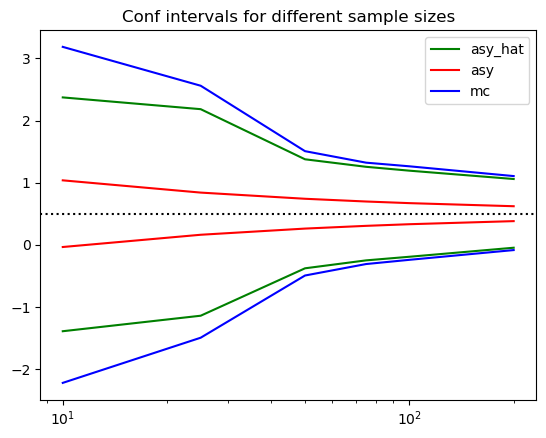

Change the error distribution to Pareto

from scipy.stats import pareto

def ols_pareto(beta,X,N,alpha):

""" Simulates the errors, estimates OLS coefficient, se, tstat and CI"""

E = np.random.pareto(alpha, N) # !!! new distribution here

Y = beta*X[0:N] + E

cov = np.cov(Y,X[0:N])

beta_hat = cov[0,1]/cov[1,1]

beta_se = (Y-beta_hat*X[0:N]).std()/(np.sqrt(N)*X[0:N].std())

tstats_asy = (beta_hat-beta)/beta_se

ci_asy = beta_hat + beta_se * np.array([-1.96,1.96])

return({'beta':beta_hat,'se':beta_se,'tstats_asy':tstats_asy,'ci_lb':ci_asy[0],'ci_ub':ci_asy[1],'N':N})

beta = 0.5

R = 10000

alpha = 3.0 # Pareto parameter

e_sd = np.sqrt(pareto.stats(alpha, moments='v'))

X = 0.2*np.random.normal(size=200)

res = [ols_pareto(beta,X,N,alpha) for _ in range(R) for N in [10,25,50,75,100,200]]

sim = pd.DataFrame(res)

sim['ci_lb_asy'] = beta - e_sd*1.96/np.sqrt(sim['N'])

sim['ci_ub_asy'] = beta + e_sd*1.96/np.sqrt(sim['N'])

sim_tmp = sim.groupby('N').mean()

sim_tmp['ub'] = sim.groupby('N')['beta'].quantile(0.975)

sim_tmp['lb'] = sim.groupby('N')['beta'].quantile(0.025)

sim_tmp = sim_tmp.reset_index()

plt.plot(sim_tmp['N'],sim_tmp['ci_lb'], color="green", label="asy_hat")

plt.plot(sim_tmp['N'],sim_tmp['ci_lb_asy'], color="red", label="asy")

plt.plot(sim_tmp['N'],sim_tmp['lb'], color="blue", label="mc")

plt.plot(sim_tmp['N'],sim_tmp['ci_ub'], color="green")

plt.plot(sim_tmp['N'],sim_tmp['ci_ub_asy'], color="red")

plt.plot(sim_tmp['N'],sim_tmp['ub'], color="blue")

plt.axhline(beta,linestyle=":",color="black")

plt.legend()

plt.title("Conf intervals for different sample sizes")

plt.xscale('log')

plt.show()

# fixme maybe an error in the red

# finite sample distribution based on normal assumption

We plotted 3 objects. The blue line is directly the (p,1-p) quantiles of the distribution of generated estimates. We can think of this as the true finite sample distribution for this particular draw of X. The red line is the asymptotic confidence interval that uses the true variance of X and the error term. Finally the green line is the average over confidence intervals across replciations generated using the asymptotic normality assumption and the sample variance of the residual.

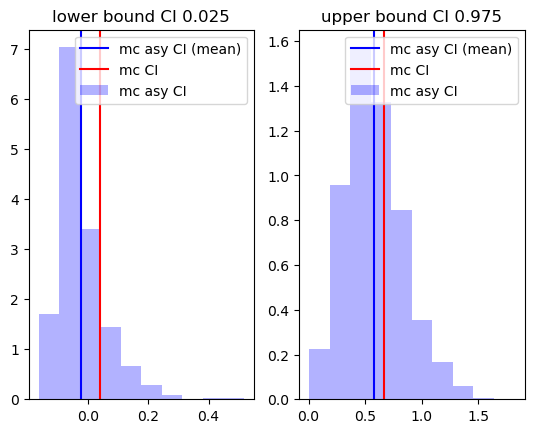

Delta method and C.I.

Let's now look at the square of \beta. From the delta method we have that

np.random.seed(10)

beta = 0.5

N = 50

R = 2000

X = np.random.normal(size=N)

# we want to compare MC CI to realized CI

ci_asy = np.zeros((R,2))

beta2_mc = np.zeros((R)) # we store the MC realizations

for i in range(R):

E = np.random.normal(size=N)

Y = beta*X + E

cov = np.cov(Y,X)

beta_hat = cov[0,1]/cov[1,1]

beta_se = (Y-beta_hat*X).std()/(np.sqrt(N)*X.std())

## we construct the estimate and the CI using the delta method

beta2_mc[i] = beta_hat ** 2

beta2_se = beta_se * 2 * np.abs(beta_hat) # see delta method formula

ci_asy[i,:] = beta_hat ** 2 + beta2_se * np.array([-1.96,1.96])

plt.subplot(1,2,1)

plt.hist(ci_asy[:,0],alpha=0.3,label="mc asy CI",color="blue",density=True)

plt.axvline( ci_asy[:,0].mean(),color="blue" ,label="mc asy CI (mean)")

plt.axvline( np.quantile(beta2_mc,0.025) ,color="red" ,label="mc CI")

plt.title("lower bound CI 0.025")

plt.legend()

plt.subplot(1,2,2)

plt.hist(ci_asy[:,1],alpha=0.3,label="mc asy CI",color="blue",density=True)

plt.axvline( ci_asy[:,1].mean(),color="blue",label="mc asy CI (mean)" )

plt.axvline( np.quantile(beta2_mc,0.975) ,color="red",label="mc CI" )

plt.legend()

plt.title("upper bound CI 0.975")

plt.show()

In particular, we note that while the Monte-Carlo CI does not include 0, and hence 0 should be rejected, the asymptotic confidence interval includes 0. In this case the asymptotic CI appears to be on average to the right of the true monte-carlo distribution across replications.

Bootstrap distribution

We create the resampling distribution and compare it to the finite sample distribution

def bootstrap_CI(Y,X,B=500):

""" Computes the CI at 0.05 percent for the OLS estimate """

N = len(Y)

beta_dm_vec_bs = np.zeros((B))

tstat_bs = np.zeros((B))

# compute the OLS estimate in the sample

cov = np.cov(Y,X)

beta_hat = cov[0,1]/cov[1,1]

beta_se_r0 = (Y-beta_hat*X).std()/(np.sqrt(N)*X.std())

beta2_se_r0 = beta_se_r0 * 2 * np.abs(beta_hat)

# bootstrap

for i in range(B):

I = np.random.randint(N,size=N)

Ys = Y[I]

Xs = X[I]

cov = np.cov(Ys,Xs)

beta_hat_r = cov[0,1]/cov[1,1] # OLS estimate for each replication

beta_dm_vec_bs[i] = beta_hat_r**2 # transformed estimate for each replciation

beta_se_r = (Ys-beta_hat_r*Xs).std()/(np.sqrt(N)*Xs.std())

beta2_se_r = beta_se_r * 2 * np.abs(beta_hat_r)

tstat_bs[i] = beta_hat_r**2 / beta2_se_r

# compute bias is any

M = np.mean(beta_dm_vec_bs)

bias = M - beta_hat**2

U = np.quantile(beta_dm_vec_bs,0.975)-bias

L = np.quantile(beta_dm_vec_bs,0.025)-bias

# U = np.quantile(beta_inv_vec_bs,0.975)

# L = np.quantile(beta_inv_vec_bs,0.025)

return(M,L,U)

np.random.seed(10)

import tqdm

all = []

for N in [50]:

R = 500 # number of replications

B = 500 # number of boostraps

X = np.random.normal(size=N)

# construct the null distribution

ci_bs = np.zeros((R,2))

ci_asy = np.zeros((R,2))

beta2_mc = np.zeros((R))

beta2_bs = np.zeros((R))

for i in tqdm.tqdm(range(R)):

E = np.random.normal(size=N)

Y = beta*X + E

cov = np.cov(Y,X)

beta_hat = cov[0,1]/cov[1,1]

beta2_mc[i] = beta_hat**2 # transformed estimate

beta_se = (Y-beta_hat*X).std()/(np.sqrt(N)*X.std())

beta2_se = beta_se * 2 * np.abs(beta_hat)

# asymptotic confidence interval using delta method

ci_asy[i,:] = beta_hat**2 + beta2_se * np.array([-1.96,1.96])

# bootstrap estimates

beta2_bs[i], ci_bs[i,0], ci_bs[i,1] = bootstrap_CI(Y,X,B)

100%|██████████| 500/500 [00:22<00:00, 22.47it/s]

plt.subplot(1,2,1)

plt.hist(ci_asy[:,0],alpha=0.3,color="blue",density=True)

plt.axvline( ci_asy[:,0].mean(),color="blue" , label="asy")

plt.axvline( np.quantile(beta2_mc,0.025) ,color="red" , label="mc CI")

plt.title("asymptotic CI 0.025")

plt.legend()

plt.subplot(1,2,2)

plt.hist(ci_asy[:,1],alpha=0.3,color="blue",density=True)

plt.axvline( ci_asy[:,1].mean(),color="blue" , label="asy")

plt.axvline( np.quantile(beta2_mc,0.975) ,color="red", label="mc CI" )

plt.title("asymptotic CI 0.975")

plt.legend()

plt.show()

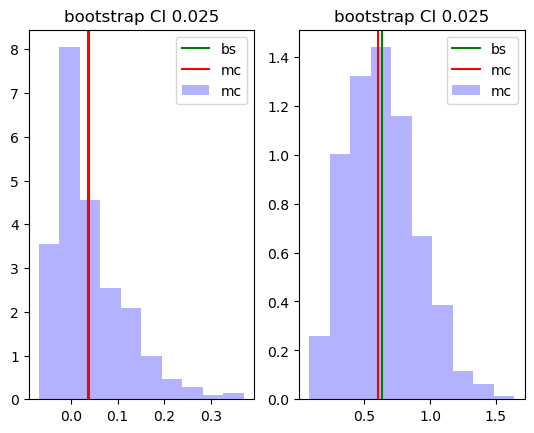

plt.subplot(1,2,1)

plt.hist(ci_bs[:,0],alpha=0.3,label="mc",color="blue",density=True)

plt.axvline( ci_bs[:,0].mean(),color="green" , label="bs")

plt.axvline( np.quantile(beta2_mc,0.025) ,color="red" , label="mc")

plt.title("bootstrap CI 0.025")

plt.legend()

plt.subplot(1,2,2)

plt.hist(ci_bs[:,1],alpha=0.3,label="mc",color="blue",density=True)

plt.axvline( ci_bs[:,1].mean(),color="green", label="bs" )

plt.axvline( np.quantile(beta2_mc,0.975) ,color="red" , label="mc")

plt.title("bootstrap CI 0.025")

plt.legend()

plt.show()

# Boostrap CI on average

ci_bs.mean(0)

array([0.03916983, 0.63744695])

# Asy CI on average

ci_asy.mean(0)

array([-0.0254555 , 0.56548982])

#

np.quantile(beta2_mc,[0.025,0.975])

array([0.03712143, 0.60464131])

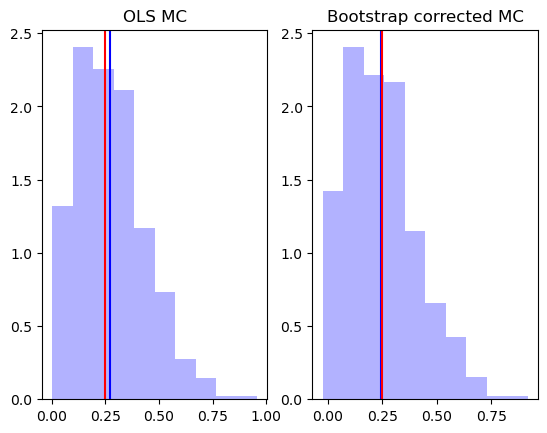

Biased in the estimate itself

We compare \beta to \beta_n to \beta^*_n. We notice for instance that \beta < \beta_n <\beta^*_n

beta**2

0.25

beta2_mc.mean()

0.2700171565383394

beta2_bs.mean()

0.29472310724131867

2*beta2_mc.mean() - beta2_bs.mean()

0.24531120583536015

plt.subplot(1,2,1)

plt.hist( beta2_mc ,alpha=0.3,label="mc",color="blue",density=True)

plt.axvline( beta2_mc.mean(),color="blue" )

plt.axvline( beta**2 ,color="red" )

plt.title("OLS MC")

plt.subplot(1,2,2)

plt.hist( 2*beta2_mc - beta2_bs ,alpha=0.3,label="mc",color="blue",density=True)

plt.axvline( (2*beta2_mc - beta2_bs).mean(),color="blue" )

plt.axvline( beta**2 ,color="red" )

plt.title("Bootstrap corrected MC")

plt.show()

A simpler exercise - Variance

Let's look at the variance estimator:

This is an consistent estimator, however we know from stat class that it is biased at finite n. We are going to look at the construction of confidence intervals based on asymptotic properties as well as bootstrap.

- link to source code for bootstrap code bootstrap

From the central limit theorem, we have in particular that:

where \mu_4 = E[ (X_i - \mu)^4].

def var_stat(X,weights=None,bias=0):

Xbar = X.mean()

Var = ( (X-Xbar)**2 ).mean()

return(Var + bias/len(X))

def F_normal(N, bs=True, bias=0):

X = np.random.normal(size=N)

varn = var_stat(X,bias=bias)

# compute asymptotic standard errors

mu = X.mean()

s2 = ( (X-mu)**2 ).mean()

mu4 = ( (X-mu)**4 ).mean()

ci_asy_lb = varn - 1.96*np.sqrt( (mu4 - s2**2)/N)

ci_asy_ub = varn + 1.96*np.sqrt( (mu4 - s2**2)/N)

return({'theta':varn,

'ci_asy_lb': ci_asy_lb,

'ci_asy_ub': ci_asy_ub,

'N':N})

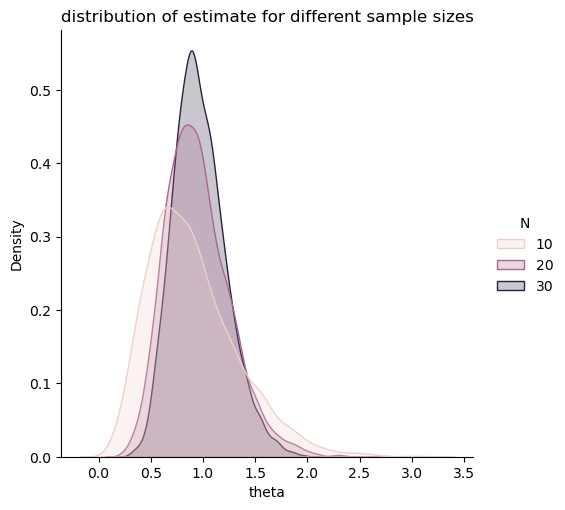

# we generate the finite sample distribution

res = [F_normal(N,False,bias=0) for N in [10,20,30,50,100,200,500,2000] for _ in range(5000)]

res = pd.DataFrame(res)

sns.displot(res.query('N<50'),x='theta',hue='N', kind="kde", fill=True)

plt.title("distribution of estimate for different sample sizes")

plt.show()

res_sum = res.groupby('N').mean()

# res_sum['lb'] = res.groupby('N')['theta'].quantile(0.025)

# res_sum['ub'] = res.groupby('N')['theta'].quantile(0.975)

res_sum['sd'] = res.groupby('N')['theta'].std()

res_sum['cov_asy'] = res.eval('c = (ci_asy_lb < 1) & (ci_asy_ub > 1) ').groupby('N').mean()['c']

res_sum

| theta | ci_asy_lb | ci_asy_ub | sd | cov_asy | |

|---|---|---|---|---|---|

| N | |||||

| 10 | 0.901047 | 0.247244 | 1.554849 | 0.433972 | 0.7438 |

| 20 | 0.946928 | 0.415006 | 1.478851 | 0.307562 | 0.8348 |

| 30 | 0.966928 | 0.508733 | 1.425123 | 0.252467 | 0.8758 |

| 50 | 0.982816 | 0.612700 | 1.352932 | 0.198106 | 0.9022 |

| 100 | 0.992174 | 0.723367 | 1.260981 | 0.141238 | 0.9270 |

| 200 | 0.995550 | 0.802543 | 1.188557 | 0.101163 | 0.9376 |

| 500 | 0.999888 | 0.876514 | 1.123263 | 0.062520 | 0.9468 |

| 2000 | 0.998711 | 0.936884 | 1.060537 | 0.031484 | 0.9524 |

From the first column we see that indeed the estimator appears consistent. We also notice that the asymptotic standard errors are centered around the point estimates by cosntruction. This means that they won't cover the parameter well in finite sample because of the bias in the parameter. They are also symetric, yet the distribution of the estimator might not be in finite sample either.

Finally, we can compute the coverage of the CI, the actual probability that it containes the parameter. We see that indeed it does converge in probability to 0.95, but that it does poorly in small sample.

Computing bootstrap Confidence Intervals

We are going to use the percentile bootstrap as well as the BC_a bootstrap.

In particular the BC_a is guaranteed to second order accurate. Meaning that its rate of convergence is one order higher than the percentile bootstrap of the asymptotic inference.

def bs_pi(X,estimator,R,bc=False):

N = len(X)

theta = np.zeros(R)

for r in range(R):

# redraw from X and apply estimator

I = np.random.randint(N,size=N)

theta[r] = estimator(X[I])

# extract CI

lb,ub = np.quantile(theta,[0.025,0.975])

if bc:

bias = np.mean(theta) - estimator(X)

lb = lb - bias

ub = ub - bias

return(lb,ub)

def F_normal(N, bs=True, bias=0, bc=False):

X = np.random.normal(size=N)

varn = var_stat(X,bias=bias)

# compute asymptotic standard errors

mu = X.mean()

s2 = ( (X-mu)**2 ).mean()

mu4 = ( (X-mu)**4 ).mean()

ci_asy_lb = varn - 1.96*np.sqrt( (mu4 - s2**2)/N)

ci_asy_ub = varn + 1.96*np.sqrt( (mu4 - s2**2)/N)

ci_pi_lb, ci_pi_ub = bs_pi(X,var_stat,500,bc=bc)

return({'theta':varn,

'ci_asy_lb': ci_asy_lb,

'ci_asy_ub': ci_asy_ub,

'ci_pi_lb': ci_pi_lb,

'ci_pi_ub': ci_pi_ub,

'N':N})

from tqdm import trange, tqdm, tqdm_notebook

import warnings

warnings.simplefilter('ignore')

R = 100

res = [F_normal(N,bc=False) for N in tqdm_notebook([10,20,30,50,75,100,200,500]) for _ in tqdm_notebook(range(R),leave=False)]

# R = 500 # repeat 20 times to compute an average

# res_bs = [F_normal(N) for N in tqdm_notebook([10,20,30,50,75,100]) for _ in tqdm_notebook(range(R),leave=False)]

# res_bs = pd.DataFrame(res_bs)

0%| | 0/8 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

res = pd.DataFrame(res)

res_sum = res.groupby('N').mean()

# res_sum['lb'] = res.groupby('N')['theta'].quantile(0.025)

# res_sum['ub'] = res.groupby('N')['theta'].quantile(0.975)

#res_sum['sd'] = res.groupby('N')['theta'].std()

res_sum['cov_asy'] = res.eval('c = (ci_asy_lb < 1) & (ci_asy_ub > 1) ').groupby('N').mean()['c']

res_sum['cov_pi'] = res.eval('c = (ci_pi_lb < 1) & (ci_pi_ub > 1) ').groupby('N').mean()['c']

res_sum

| theta | ci_asy_lb | ci_asy_ub | ci_pi_lb | ci_pi_ub | cov_asy | cov_pi | |

|---|---|---|---|---|---|---|---|

| N | |||||||

| 10 | 0.922611 | 0.232453 | 1.612768 | 0.246309 | 1.524426 | 0.79 | 0.76 |

| 20 | 0.915490 | 0.391975 | 1.439004 | 0.415024 | 1.412330 | 0.85 | 0.84 |

| 30 | 0.966602 | 0.515642 | 1.417563 | 0.532244 | 1.405382 | 0.88 | 0.87 |

| 50 | 0.994769 | 0.623759 | 1.365779 | 0.636390 | 1.358784 | 0.93 | 0.93 |

| 75 | 1.000314 | 0.690987 | 1.309641 | 0.703829 | 1.310524 | 0.90 | 0.90 |

| 100 | 0.985057 | 0.715681 | 1.254434 | 0.724286 | 1.254821 | 0.94 | 0.92 |

| 200 | 1.006862 | 0.816019 | 1.197706 | 0.823206 | 1.196777 | 0.95 | 0.95 |

| 500 | 1.002962 | 0.878143 | 1.127781 | 0.882316 | 1.128654 | 0.96 | 0.95 |

We see here that the percentile boostrap doesn't provide much of an advantage when compared to the asymptotic confidence interval. We then turn to the BCa bootstrap.

Call \theta^*(r) the different bootstrap replications. The percentile boostrap simply computes the 0.025 and 0.975 quantiles in this replicated distribution.

The BCa approach, on the other hand uses adjusted quantiles. It uses:

where z and a are computed from the replications. For instance

the acceleration a has to do with higher order moments of the distribution of replications.

Importantly, the BCa conf interval can be shown to be second order accurate. While we usually have that

For the BCa it is the case that

np.random.seed(234453)

def F_normal(N, bs=True, bias=0):

X = (1/0.6)*np.abs(np.random.normal(size=N))

#X = np.random.normal(size=N)

#X = np.random.pareto(5.0, N) # !!! new distribution here

varn = var_stat(X,bias=bias)

# compute asymptotic standard errors

mu = X.mean()

s2 = ( (X-mu)**2 ).mean()

mu4 = ( (X-mu)**4 ).mean()

ci_asy_lb = varn - 1.96*np.sqrt( (mu4 - s2**2)/N)

ci_asy_ub = varn + 1.96*np.sqrt( (mu4 - s2**2)/N)

# boostrap

ci_pi_lb, ci_pi_ub = bs_pi(X,var_stat,2000)

bs_bca = boot.ci(X, var_stat, method="bca", n_samples=2000)

return({'theta':varn,

'ci_asy_lb': ci_asy_lb,

'ci_asy_ub': ci_asy_ub,

'ci_pi_lb': ci_pi_lb,

'ci_pi_ub': ci_pi_ub,

'ci_bca_lb': bs_bca[0],

'ci_bca_ub': bs_bca[1],

'N':N})

R = 100 # number of sample replciations (not the number of draws in bootstrap)

res = [F_normal(N) for N in tqdm_notebook([10,20,30,50,75,100,200,500]) for _ in tqdm_notebook(range(R),leave=False)]

#res = [F_normal(N) for N in tqdm_notebook([500]) for _ in tqdm_notebook(range(R),leave=False)]

res = pd.DataFrame(res)

0%| | 0/8 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

0%| | 0/100 [00:00<?, ?it/s]

res_sum = res.groupby('N').mean()

res_sum['lb'] = res.groupby('N')['theta'].quantile(0.025)

res_sum['ub'] = res.groupby('N')['theta'].quantile(0.975)

res_sum['sd'] = res.groupby('N')['theta'].std()

res_sum['cov_asy'] = res.eval('c = (ci_asy_lb < 1) & (ci_asy_ub > 1) ').groupby('N').mean()['c']

res_sum['cov_pi'] = res.eval('c = (ci_pi_lb < 1) & (ci_pi_ub > 1) ').groupby('N').mean()['c']

res_sum['cov_bca'] = res.eval('c = (ci_bca_lb < 1) & (ci_bca_ub > 1) ').groupby('N').mean()['c']

#res_sum['cov_abc'] = res.eval('c = (ci_abc_lb < 1) & (ci_abc_ub > 1) ').groupby('N').mean()['c']

res_sum

| theta | ci_asy_lb | ci_asy_ub | ci_pi_lb | ci_pi_ub | ci_bca_lb | ci_bca_ub | lb | ub | sd | cov_asy | cov_pi | cov_bca | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | |||||||||||||

| 10 | 0.869517 | 0.174061 | 1.564974 | 0.202859 | 1.453777 | 0.354924 | 1.755925 | 0.211509 | 1.918902 | 0.450517 | 0.68 | 0.67 | 0.75 |

| 20 | 0.900818 | 0.365291 | 1.436345 | 0.386892 | 1.405077 | 0.508638 | 1.676115 | 0.423087 | 1.625944 | 0.340470 | 0.74 | 0.71 | 0.82 |

| 30 | 0.987153 | 0.462526 | 1.511781 | 0.490699 | 1.501187 | 0.597912 | 1.750266 | 0.477577 | 1.742428 | 0.317701 | 0.83 | 0.82 | 0.86 |

| 50 | 0.987274 | 0.560474 | 1.414073 | 0.581286 | 1.413819 | 0.664168 | 1.591834 | 0.619902 | 1.417006 | 0.209673 | 0.93 | 0.93 | 0.93 |

| 75 | 0.996387 | 0.638414 | 1.354359 | 0.656981 | 1.359801 | 0.719417 | 1.492791 | 0.677484 | 1.392168 | 0.190277 | 0.89 | 0.89 | 0.92 |

| 100 | 0.994734 | 0.679935 | 1.309534 | 0.697178 | 1.316708 | 0.751731 | 1.427705 | 0.659599 | 1.400612 | 0.198564 | 0.87 | 0.87 | 0.91 |

| 200 | 1.025432 | 0.790483 | 1.260380 | 0.800097 | 1.266053 | 0.833182 | 1.323666 | 0.812848 | 1.273392 | 0.129253 | 0.93 | 0.93 | 0.92 |

| 500 | 0.988418 | 0.843802 | 1.133034 | 0.847192 | 1.135461 | 0.863119 | 1.155419 | 0.839146 | 1.121996 | 0.074282 | 0.92 | 0.92 | 0.92 |

We can also look at the shape of the interval

res_sum = res.groupby('N').mean()

res_sum['lb'] = res.groupby('N')['theta'].quantile(0.025)

res_sum['ub'] = res.groupby('N')['theta'].quantile(0.975)

res_sum['sd'] = res.groupby('N')['theta'].std()

res_sum['cov_asy'] = res.eval('c = (ci_asy_lb < 1) & (ci_asy_ub > 1) ').groupby('N').mean()['c']

res_sum['cov_pi'] = res.eval('c = (ci_pi_lb < 1) & (ci_pi_ub > 1) ').groupby('N').mean()['c']

res_sum['cov_bca'] = res.eval('c = (ci_bca_lb < 1) & (ci_bca_ub > 1) ').groupby('N').mean()['c']

#res_sum['cov_abc'] = res.eval('c = (ci_abc_lb < 1) & (ci_abc_ub > 1) ').groupby('N').mean()['c']

res_sum

| theta | ci_asy_lb | ci_asy_ub | ci_pi_lb | ci_pi_ub | ci_bca_lb | ci_bca_ub | lb | ub | sd | cov_asy | cov_pi | cov_bca | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | |||||||||||||

| 10 | 0.869517 | 0.174061 | 1.564974 | 0.202859 | 1.453777 | 0.354924 | 1.755925 | 0.211509 | 1.918902 | 0.450517 | 0.68 | 0.67 | 0.75 |

| 20 | 0.900818 | 0.365291 | 1.436345 | 0.386892 | 1.405077 | 0.508638 | 1.676115 | 0.423087 | 1.625944 | 0.340470 | 0.74 | 0.71 | 0.82 |

| 30 | 0.987153 | 0.462526 | 1.511781 | 0.490699 | 1.501187 | 0.597912 | 1.750266 | 0.477577 | 1.742428 | 0.317701 | 0.83 | 0.82 | 0.86 |

| 50 | 0.987274 | 0.560474 | 1.414073 | 0.581286 | 1.413819 | 0.664168 | 1.591834 | 0.619902 | 1.417006 | 0.209673 | 0.93 | 0.93 | 0.93 |

| 75 | 0.996387 | 0.638414 | 1.354359 | 0.656981 | 1.359801 | 0.719417 | 1.492791 | 0.677484 | 1.392168 | 0.190277 | 0.89 | 0.89 | 0.92 |

| 100 | 0.994734 | 0.679935 | 1.309534 | 0.697178 | 1.316708 | 0.751731 | 1.427705 | 0.659599 | 1.400612 | 0.198564 | 0.87 | 0.87 | 0.91 |

| 200 | 1.025432 | 0.790483 | 1.260380 | 0.800097 | 1.266053 | 0.833182 | 1.323666 | 0.812848 | 1.273392 | 0.129253 | 0.93 | 0.93 | 0.92 |

| 500 | 0.988418 | 0.843802 | 1.133034 | 0.847192 | 1.135461 | 0.863119 | 1.155419 | 0.839146 | 1.121996 | 0.074282 | 0.92 | 0.92 | 0.92 |

res_sum.eval("width = ub-lb").eval("width_asy = ci_asy_ub-ci_asy_lb").eval("width_bca = ci_bca_ub-ci_bca_lb")

| theta | ci_asy_lb | ci_asy_ub | ci_pi_lb | ci_pi_ub | ci_bca_lb | ci_bca_ub | lb | ub | sd | cov_asy | cov_pi | cov_bca | width | width_asy | width_bca | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ||||||||||||||||

| 10 | 0.869517 | 0.174061 | 1.564974 | 0.202859 | 1.453777 | 0.354924 | 1.755925 | 0.211509 | 1.918902 | 0.450517 | 0.68 | 0.67 | 0.75 | 1.707393 | 1.390913 | 1.401001 |

| 20 | 0.900818 | 0.365291 | 1.436345 | 0.386892 | 1.405077 | 0.508638 | 1.676115 | 0.423087 | 1.625944 | 0.340470 | 0.74 | 0.71 | 0.82 | 1.202857 | 1.071054 | 1.167477 |

| 30 | 0.987153 | 0.462526 | 1.511781 | 0.490699 | 1.501187 | 0.597912 | 1.750266 | 0.477577 | 1.742428 | 0.317701 | 0.83 | 0.82 | 0.86 | 1.264851 | 1.049255 | 1.152354 |

| 50 | 0.987274 | 0.560474 | 1.414073 | 0.581286 | 1.413819 | 0.664168 | 1.591834 | 0.619902 | 1.417006 | 0.209673 | 0.93 | 0.93 | 0.93 | 0.797105 | 0.853599 | 0.927665 |

| 75 | 0.996387 | 0.638414 | 1.354359 | 0.656981 | 1.359801 | 0.719417 | 1.492791 | 0.677484 | 1.392168 | 0.190277 | 0.89 | 0.89 | 0.92 | 0.714684 | 0.715945 | 0.773374 |

| 100 | 0.994734 | 0.679935 | 1.309534 | 0.697178 | 1.316708 | 0.751731 | 1.427705 | 0.659599 | 1.400612 | 0.198564 | 0.87 | 0.87 | 0.91 | 0.741013 | 0.629599 | 0.675975 |

| 200 | 1.025432 | 0.790483 | 1.260380 | 0.800097 | 1.266053 | 0.833182 | 1.323666 | 0.812848 | 1.273392 | 0.129253 | 0.93 | 0.93 | 0.92 | 0.460544 | 0.469897 | 0.490484 |

| 500 | 0.988418 | 0.843802 | 1.133034 | 0.847192 | 1.135461 | 0.863119 | 1.155419 | 0.839146 | 1.121996 | 0.074282 | 0.92 | 0.92 | 0.92 | 0.282851 | 0.289232 | 0.292299 |

We want to think about whether the finite sample distribution is symetric around the estimates. We can first look at the dsitribution in realizeded valued.

plt.hist(res.query("N==20")['theta'],alpha=0.3)

plt.axvline(x=1.0,color="red")

plt.axvline(x=res.query("N==20")['theta'].mean())

plt.axvline(x=res.query("N==20")['theta'].quantile(0.025),linestyle=":")

plt.axvline(x=res.query("N==20")['theta'].quantile(0.975),linestyle=":")

<matplotlib.lines.Line2D at 0x7f098d168f10>

From this we see that when constructing the CI around the estimate, we might not want to use a symetric distribution. The bootstrap can help with that since it picks up the non symmetry through the replication. We can check if the bootstrap is able to reproduce such shape due to finite sample issues.

res.eval("shape_bca = (ci_bca_ub - theta)/(theta - ci_bca_lb)").groupby('N')['shape_bca'].mean()

N

10 1.756288

20 1.904075

30 1.925115

50 1.835687

75 1.742245

100 1.749908

200 1.540531

500 1.334661

Name: shape_bca, dtype: float64

res.eval("shape_bca = (ci_pi_ub - theta)/(theta - ci_pi_lb)").groupby('N')['shape_bca'].mean()

N

10 0.849145

20 0.953922

30 1.015952

50 1.038469

75 1.054027

100 1.070927

200 1.063228

500 1.041023

Name: shape_bca, dtype: float64

res.eval("shape_bca = (ci_asy_ub - theta)/(theta - ci_asy_lb)").groupby('N')['shape_bca'].mean()

N

10 1.0

20 1.0

30 1.0

50 1.0

75 1.0

100 1.0

200 1.0

500 1.0

Name: shape_bca, dtype: float64

res_sum = res.groupby('N').mean()

res_sum['lb'] = res.groupby('N')['theta'].quantile(0.025)

res_sum['ub'] = res.groupby('N')['theta'].quantile(0.975)

res_sum.eval("shape = (ub -theta)/(theta - lb)")

| theta | ci_asy_lb | ci_asy_ub | ci_pi_lb | ci_pi_ub | ci_bca_lb | ci_bca_ub | lb | ub | shape | |

|---|---|---|---|---|---|---|---|---|---|---|

| N | ||||||||||

| 10 | 0.869517 | 0.174061 | 1.564974 | 0.202859 | 1.453777 | 0.354924 | 1.755925 | 0.211509 | 1.918902 | 1.594790 |

| 20 | 0.900818 | 0.365291 | 1.436345 | 0.386892 | 1.405077 | 0.508638 | 1.676115 | 0.423087 | 1.625944 | 1.517855 |

| 30 | 0.987153 | 0.462526 | 1.511781 | 0.490699 | 1.501187 | 0.597912 | 1.750266 | 0.477577 | 1.742428 | 1.482165 |

| 50 | 0.987274 | 0.560474 | 1.414073 | 0.581286 | 1.413819 | 0.664168 | 1.591834 | 0.619902 | 1.417006 | 1.169749 |

| 75 | 0.996387 | 0.638414 | 1.354359 | 0.656981 | 1.359801 | 0.719417 | 1.492791 | 0.677484 | 1.392168 | 1.241073 |

| 100 | 0.994734 | 0.679935 | 1.309534 | 0.697178 | 1.316708 | 0.751731 | 1.427705 | 0.659599 | 1.400612 | 1.211083 |

| 200 | 1.025432 | 0.790483 | 1.260380 | 0.800097 | 1.266053 | 0.833182 | 1.323666 | 0.812848 | 1.273392 | 1.166415 |

| 500 | 0.988418 | 0.843802 | 1.133034 | 0.847192 | 1.135461 | 0.863119 | 1.155419 | 0.839146 | 1.121996 | 0.894860 |